Debt Relief – How to Pay Your Bills if You Have Lost Your Job

Debt Relief In An Uncertain Time

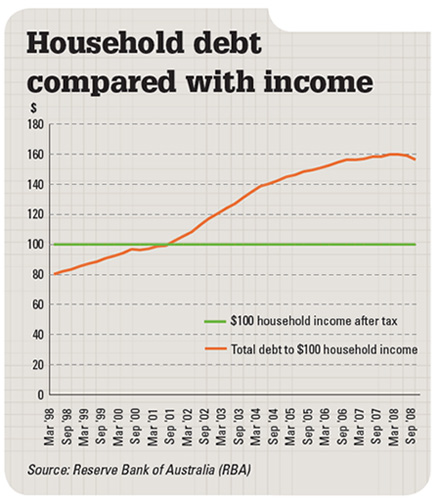

Debt relief in these economically uncertain times is one of the biggest hurdles facing Australians. In recent years we have watched as unemployment rates rise and household debts climb higher and higher.

It is estimated that most households now owe more then twice what we did just ten years ago. It comes out to an average of $160 of debt for every $100 we make after taxes. Those numbers are clearly a disaster waiting to happen.

In many extreme cases consumers carry up to $400,000 in credit card debt spread out over forty or fifty cards. Of the cards that we all have in our wallets a staggering 75% are not paid off each month.

These same cards accrue interest at rates hovering near 20% on average balances of over two thousand dollars.

There are some bright spots on the horizon, mostly a noted improvement in our fellow citizens commitment to reducing debt.

Some debt relief companies have also seen a move towards saving more money in preparation for whatever difficult trials the economy throws at us next.

If you are one of the people who wants to get out of debt, even if you are unemployed there is hope. One of the first options to look at are financial counsellors.

Financial counselling is a free service that can help you figure out your options and learn how to control spending.

Another option that is often referenced is debt relief companies. But, consumers should be aware that these companies are known for getting consumers into debt agreements that will negatively impact your credit history and wind up costing more money rather then less.

Debt Relief Steps

- Evaluate or come up with a budget – There are loads of ways to reduce your expenses like selling as second car or cutting back on entertainment costs. You can also increase your income by taking on a second job or taking in a boarder.

- Ask for Advice – Although it might feel like it, you are not the only person facing budget problems. Ask your friends and family what they do to cut costs and increase income. Scour the Internet for helpful websites concerning debt relief.

- Pay extra – This is not an easy option, but once you have cut costs and/or earned more money use it to make extra payments on your credit cards or mortgage. In the long run it can save you thousands of dollars in interest.

Choosing Debt Relief

If you, like a lot of Australians are worried about your employment you need to start planning now for the worst case scenario.

If you start to evaluate and plan now things will be much easier should your job situation change or you are briefly unemployed.

Those who are already in financial trouble or are unemployed need to work quickly to deal with their debt. You should immediately contact your creditors so they know you are having a problem rather then that you are just skipping out on your bill.

You should also enlist the help of a debt counsellor right away. If you wait until you are way behind on your bills you will have less choice in how your debt is handles.

Also, resist the urge to do things that exacerbate the problem like paying your credit card bill or mortgage with another credit card. This will only make matters worse and increase your debt astronomically.

Instead, look into applying for short term debt relief, remember your creditors do not want you to default on your bills either.

It is better for you and them to work out a plan that meets your needs and pays off your bills. Just keep in mind that it is not a magic fix.

Debt relief options could be costly and damage your credit so make sure you have tried every other avenue prior to taking this step.

Getting Debt Relief Help

In Australia the Big Four banks have announced that if a borrower loses their job they could be considered for a debt relief holiday for up to twelve months.

This is an indication that lenders are feeling the pinch too and are more willing then ever to help you meet your payment responsibilities.

If you do not qualify for a full holiday you might be able to increase the length of your loan to reduce payments or make interest only payments until you are back on your feet.

Credit cards can be dealt with by asking the issuer to switch you to a lower interest card or to take out a personal loan to pay off the card debt.

A personal loan will carry significantly less interest and probably have a lower monthly payment. If you do either of these options you should immediately shred your credit card and use cash or a debit card in its place.

How To Pay Your Bills

Whether you are behind or think you are in danger of getting behind your first line of defense should be financial counselling services.

These independent counsellors provide free assistance to help you manage your money and control your debt. They will also help you by negotiating with your lender on your behalf, however they usually suggest that you make an attempt first.

By doing some of the negotiations yourself you can feel better about how your debt is being handled and more in control of your own destiny.

Where To Get Help To Pay Your Bills

There are services available for almost any situation. If you are caught up in debt or are unemployed check out these services.

Energy Bill Debt Relief

Most energy retailers have a flexible payment option. Contact them first to see what choices they offer. In some cases you might be able to get government assistance. Contact your local fair trading or consumer affairs branch.

Tax Bill Debt Relief

If you have serious debt problems and need relief from all or part of your tax liability contact the Australian Taxation Office. They can delay or relieve your debt payment. Visit www.ato.gov.au for more information.

StepUP Loan For Debt Relief

The StepUp Loan is a low interest personal loan developed by Good Shepherd Youth and Family Service and NAB. Anyone who has a health card or get Family Tax Benefit Part

A may be eligible for a loan between $800 and $3000 at a fixed rate of 3.99%. There are no additional fees and repayment options are highly flexible.

The money must be used to purchase home furnishings, computer equipment or a used vehicle. More information is available at www.goodshepvic.org/au/microfinance.

No-Interest Loan For Debt Relief

In Australia there are 280 community organisations that offer interest- free loans. These are not in store loans or financing.

They are made by community organisations specifically to pay for household goods or medical equipment. Anyone who carries a health care or pension card and has a low income is eligible.

The loans range from $800 to $1200 and are repaid over one year to eighteen months. Visit the www.goodshepvic.org.au/microfinance for more information on these loans.

Early Super Release

If you meet certain criteria you may qualify to access a portion or all of your superannuation money.

This only makes sense in you are in a short term debt problem and there are many risks involved including losing your superannuation for good or losing your home. Visit www.apra.gov.au to explore this option.

Example: Living Beyond Your Means

Many Australians can probably relate to the issues faced by the fictional couple Bill and Sue. They are a married couple in their mid 30′s with two children who both worked.

Bill’s employer was forced to cut expenses and cut his pay which amounted to half of his income. At the same time the economy forced Sue to shutter the windows on her small business. They had a debt of $40,000 in personal loans and credit cards.

To help deal with the debt relief problem they enlisted the help of a debt relief counsellor. She helped them make a budget that provided them with real numbers on their pre debt repayment living costs.

These numbers showed them that even without paying any money toward the debt they were spending more then they made.

The first thing they needed to do was deal with their income and their expenses. Sue chose to file bankruptcy on the costs of her business while Bill worked out a hardship payment plan on their debts. While Sue’s credit file took a hit, Bill was able to maintain his which helped them to feel better about meeting their goal of someday owning a home.

The Perils of a Debt Agreement

A debt agreement is a binding contract between you and your creditors wherein they agree to accept the amount that you can afford to pay.

To be eligible for one of these agreements you must be unable to pay your debts at their due date and have an after tax income of less then $61,875.

Further you can’t owe more then $82,500 in unsecured debt nor can your assets add up to more then that amount.

In these agreements the debts freeze, which means they no longer earn interest and you agree to pay a specified amount each week for the next three to five years.

A debt agreement administrator is typically the person that negotiates your plan. They will work with lenders to come up with a budget plan to pay off the amount you owe.

However, it is a well known problem that these administrators set up plans that are often not realistic which causes borrowers to default on the debt agreement.

It is of the utmost importance that you go through all the details of your agreement and budget to make sure it correctly reflects your situation and has realistic goals.

Any debt agreement must be lodged with the Insolvency and Trustee Services Australia as well as a majority of your unsecured creditors. All parties have to agree or it is not binding.

On average you will be required to pay back between 75% and 25% of your debt in addition to a set up fee of $2000 and an administration fee.

This fee is usually 20% of the total owed amount and is paid to the administrator of the debt agreement. The government will also charge a fee of 3.5% of the amount owed.

Remember too that debt agreements are not for secured loans like mortgages or auto loans. Should you default on those loans your home or vehicle could be repossessed.

The debt agreement loan is only for personal loans or credit card debts. If you default on your repayment agreement you could be forced to file bankruptcy by your creditors.

Bankruptcy For Debt Relief

Bankruptcy is an expensive way to relieve debt. While it frees you from all of your payments it also allows the creditors to take anything you earn or acquire for three years.

Any assets you have or earn will be sold to repay your creditors. This includes any inheritance you may receive during the three year bankruptcy period.

You will also have to repay 50% of your after tax income about $41,250 for a single person. You will not be able to have a job that requires a licence or involved dealing with money.

You will also have to get permission from your trustee to travel abroad. Visit www.itsa.gov.au for more information on bankruptcy.

Example: Dealing With A Debt Administrator

Bethany is a working mother of two and a wife who has found herself in mounting debt. She contacts a debt administrator for help with her situation.

In total she has three credit cards with debt near $69,000 and a joint card loan with her husband as well as one in her own name.

The car loans are secured and therefore not applicable to a debt agreement. The administrator negotiated for her and comes up with a bill of $48,000.

Of this she will spend $36,000 to repay her creditors, $10,400 for her account set up fee to the debt administrator and $2,600 for the government charge

She agrees to pay back the money over three years at a rate of about $250 which will increase to about $300 once she pays off one of the card loans.

The payments leave only enough money for Bethany and her husband to meet their rent payment, food, and the car loans.

Other costs like school trips and dining out will be difficult to cover under these terms. Should they fail to meet the requirements the creditors could get an order to force them into bankruptcy.

Sneaky Tactics

Debt Agreement Administrators or Debt Relief companies claim that their goal is to help you find an agreement that meets your needs.

Often they recommend bankruptcy or other options for a fee. In order to see how they really operate the an Australian consumer advocacy website had two people call and explain their debt situation to see what responses they would get.

While the two different callers claimed to have strikingly similar financial profiles they had different levels of debt.

Both said their pre tax income was $40,000 and they were single with no dependents. Each claimed to be renting a small apartment in an outer suburb of Sydney.

They also claimed to be behind by three payments and to have no other assets aside from their vehicles, superannuation funds, and average household items. Neither had any significant assets or money in savings.

Caller number one said she had to credit cards with just under $12,000 on them and a recent expenditure of $3,000 for an unexpected repair. Her car was valued at $6000.

Caller number two said she had four cards with a balance of around $27,000 and a secure auto loan of $11,000 for a vehicle valued at $8,000. She had been unemployed but had recently gotten a job.

Interesting Findings

Both callers got advice on using a debt agreement to get out of debt. While there were other suggestions made about negotiating with the lender, refinancing, or requesting a hardship variation none of the debt administrators suggested the callers seek the assistance of a debt counsellor.

Both conversations were relatively short with the administrator spending only about 15 minutes with each caller.

In most cases the phone consultant requested debt information from the callers about their situation and income.

However, one company did ask to have all financial information submitted and was then told that the agreement would require her to put all of her money in a trust with the company and then they would send her money to live on each week.

It is clear how dangerous this choice would have been, considering the risk of problems if the company neglected to send her enough money to live on. In addition most of the companies were unable to or did not quote fees ongoing fees.

A Financial Counsellors Assessment

The same information on the callers debts was given to a financial counsellor. His assessment was quite different from that of the debt administrator..

Caller Number One – Considering the high cost of debt agreement it is not a good choice for caller number one. Since she only has two creditors she should contact them to try and negotiate a lower interest rate.

She might also try to consolidate the two cards into a more manageable personal loan at a lower and fixed interest rate.

This caller should also look at ways to make more money to put aside for unexpected costs, instead of leaning on credit cards. A second job or renting out the extra bedroom in her apartment were some of his recommendations.

Caller Number Two – This caller has two viable options; bankruptcy or a hardship variation. A bankruptcy would allow her to have a new start and protect her from repayments should she again become unemployed.

If she managed to keep up the payments on her vehicle the lender might let her keep it in spite of the bankruptcy.

She could also claim hardship due to her previous unemployment or argue maladministration. This claim means that she believed she was lent more money then she should have been based on her income.

If the lenders refused to grant the hardships or reduce the debt she could file a complaint with the ombudsman.

Your Have Debt Relief Rights Under The Consumer Code

The Uniform Consumer Credit Code is intended to help figure out how to pay your bills when your debt gets out of control through no fault of their own.

Becoming unemployed, illness, or family disruption are some of the reasons you can use to renegotiate your debts. However, you mist act quickly to make an application for hardship variation or your loan.

Section 25 of the Code of Banking Practice says, “We will try to help you overcome you We will try to help you overcome your financial difficulties with any credit facility you have with us.

We could, for example, work with you to develop a repayment plan.’ This will help you if you are in debt to a bank.

Too often people try to deal with debt by going into more debt with credit cards and loans rather then asking for help. Once they can no longer borrow money or get credit their only choice is bankruptcy.

Contact your lender right away when you have a problem and ask if you can apply for temporary relief. They may waive fees or interest or reduce your minimum payment.

Be sure to offer to make payments that you can afford after you have covered your regular living expenses and other debts.

The lender will have a procedure in place to assess your application. If your lender refuses complain to the Credit or Financial Ombudsman Service, free to all consumers.

You may also opt to have your case heard by the state court or tribunal. However, lenders are trying to be fair and are increasingly likely to help you manage your debt.